Why is the observation of physical inventory a mandatory procedure

Christopher Anderson

Published Mar 29, 2026

Observing physical inventory is a key step in meeting the required standard of field work. It also gives information and proof that it was done correctly and numbers are accurate. Auditors check to make sure that inventory is: real, quantity is accurate and it is in usable condition!

What are the purposes of the auditors observation of the taking of the physical inventory?

The primary reason auditors observe their client taking the physical inventory is to make sure the inventory reflected on the balance sheet actually exists and that the balance sheet includes all inventory owned by the company.

Why does the auditor perform inventory test counts and trace these items to the inventory records?

The auditors want to be comfortable with the procedures you use to count the inventory. … They will trace the valuation compiled from the physical inventory count to the company’s general ledger, to verify that the counted balance was carried forward into the company’s accounting records. Test high-value items.

What are inventory observations?

An inventory observation is the oversight of a client’s inventory counting process by an outside auditor. This oversight work includes a number of tasks, including the following: Verifying that all inventory was counted. Testing a sample of the counts made by client employees.Which of the following statements is true regarding the use of remittance advices?

Which of the following statements is true regarding the use of remittance advices? Remittance advices are used to record sales. If remittance advices are not used, the balance of accounts receivable could be misstated. If remittance advices are not used, the allowance for doubtful accounts could be misstated.

What major purpose is served by requiring the auditor to observe the client's physical inventory count?

Observing physical inventory is a key step in meeting the required standard of field work. It also gives information and proof that it was done correctly and numbers are accurate. Auditors check to make sure that inventory is: real, quantity is accurate and it is in usable condition!

Why do we perform substantive procedures?

Substantive procedures are intended to create evidence that an auditor assembles to support the assertion that there are no material misstatements in regard to the completeness, validity, and accuracy of the financial records of an entity.

Why are physical audits necessary?

An inventory audit, particularly the physical count part of the process, can help teams ensure appropriate inventory levels, identify inefficiencies and budget more accurately. It can also help identify more nefarious activities, like theft, as well as damaged or forgotten goods.Why is inventory observation important?

Importance of Auditing Inventory Observation of inventory is a generally accepted auditing procedure, where an independent auditor issues an opinion on whether the financial records of inventory accurately represent the physical inventory being carried.

What is the main objective of observing inventory?Objective of inventory observation: This is to ensure that there is no conflict of interest involved. However, during the counting process, the auditor might request to recount certain items that are noted as unusual by them.

Article first time published onWhy would an auditor choose to perform analytical procedures on inventory?

It’s important to conduct inventory audits to maintain inventory accuracy, spot causes of shrinkage, and ensure that you always have the right amount of stock at the right time. A better understanding of stock flow will also help ensure the business runs smoothly, because you’ll know what products you have on hand.

Why is auditing inventory important?

Inventory audit is necessary to reduce unnecessary investment in stocks and to ensure that you have a proper line balancing in the process. … High levels of stock generally result in unnecessary overstocking thus resulting in poor cash flows and financial loss.

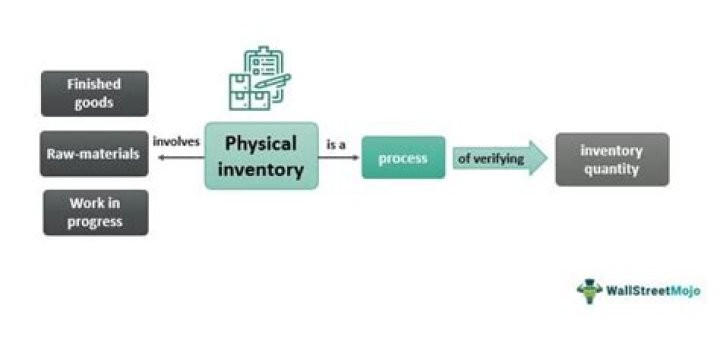

What is physical count of inventory?

A physical inventory count is a structured approach to counting a company’s stock where staff uses a predetermined method to count the goods. Companies schedule a physical inventory count at the end of a reporting period.

Why is remittance advice important?

A remittance advice helps in maintaining records and is beneficial for the customers who pay through cheque. It helps the receiver of remittance advice to compare the amount of payment sent by the buyer with the actual due amount.

What is the purpose of remittance advice?

A remittance advice is a document which provides a breakdown of the invoices included on a payment. It is sent from a customer to a supplier letting the supplier know they have paid their invoice. In it’s simpliest form it shows the invoice number and payment amount sent or enclosed.

What is the difference between an explanation of benefits and a remittance advice?

Both types of statements provide an explanation of benefits, but the remittance advice is provided directly to the health-care provider, whereas the explanation of benefits statement is sent to insured patient, according to Louisiana Department of Health.

How do we use substantive analytical procedures?

- STEP 1: Develop an independent expectation. …

- STEP 2: Define a significant difference (or threshold) …

- STEP 3: Compute difference. …

- STEP 4: Investigate significant differences and draw conclusions.

What is substantive procedure?

A substantive procedure is a process, step, or test that creates conclusive evidence regarding the completeness, existence, disclosure, rights, or valuation (the five audit assertions) of assets and/or accounts on the financial statements.

What are the substantive procedures for inventory?

Substantive procedures Obtain a copy of the inventory listing and agree the total to the general ledger and the financial statements. During the inventory count select a sample of goods physically present in the warehouse and confirm recorded in the inventory records.

Are inventory counts required?

According to the IRS and generally accepted accounting principles (“GAAP”), companies with physical inventory are required to, periodically, conduct an inventory count. … Full annual inventory counting is not as popular as it had been in the past, but still may be ideal for companies with smaller quantities of inventory.

What are the auditor's responsibilities regarding inventory when it is determined solely by a physical count?

When inventory quantities are determined solely by means of a physical count, and all counts are made as of the balance-sheet date or as of a single date within a reasonable time before or after the balance-sheet date, it is ordinarily necessary for the independent auditor to be present at the time of count and, by …

How does an auditor verify inventories?

Auditors often perform this inventory audit at random. It involves matching the cost of inventory shipped with the number of products shipped. It verifies that no products are shipped for the incorrect amount of money.

What kinds of information about inventory can be obtained through substantive analytical procedures?

For all levels of risk of material misstatement, analytical procedures normally performed for inventories would include: Compare account balances in purchases, inventories and costs of good sold accounts with the preceding year or years. Investigate significant changes in amounts or deviations from trends.

What are the procedures typically to be performed by to achieve audit program for inventories and cost of goods sold?

Consider internal control over inventories and cost of goods sold. Determine the existence of inventories and the occurrence of transactions affecting cost of goods sold. Establish the completeness of inventories. Establish that the client has right to the recorded inventories.

Why does inventory represent one of the more complex parts of the audit?

Why does inventory represent one of the more complex parts of the audit? Assigning costs to value inventory can be difficult and there may be other troublesome valuation issues such as obsolescence and lower of cost or market. The acquisition and payment for inventory is controlled by purchasing.

Why inventory stock valuation and the year end inventory count are important to the audit of financial statements?

In the audit process of inventory, physical inventory count may be the most important part of the inventory audit. This is due to physical inventory count can provide evidence on existence and completeness. … The misstatement on inventory not only affects the balance sheet but also the income statement.

How do you audit inventory from a warehouse?

- Define your objectives.

- Conduct warehouse inventory counts.

- Observe warehouse operations.

- Interview key warehouse employees.

- Synthesize inventory data.

- Evaluate the inventory audit results.

Which audit procedure is most reliable?

Physical Inspection Physical examinations are useful procedures for auditing assertions because they provide highly reliable audit evidence regarding the existence of assets. Inspections go beyond merely scrutinizing the supporting documents.

Why do we perform test of controls?

The aim of tests of control in auditing is to determine whether these internal controls are sufficient to detect or prevent risks of material misstatements. … However, if they are found to be weak or ineffective, the control risk is high. This means that the auditor will have to perform additional tests during the audit.

What is audit procedure?

Audit procedures are the processes and methods auditors use to obtain sufficient, appropriate audit evidence to give their professional judgment about the effectiveness of an organization’s internal controls.

What information should the auditor obtain during the physical count to ensure that cut off for sales is accurate?

The auditor should examine the way the inventory count is organised and evaluate the adequacy of management’s instructions; for example as to whether they address the accurate identification of slow-moving, obsolete or damaged items or control over the shipping and receipt of inventory before and after the cut-off date …