What if errors are serially correlated?

Sarah Cherry

Published Feb 27, 2026

What if errors are serially correlated?

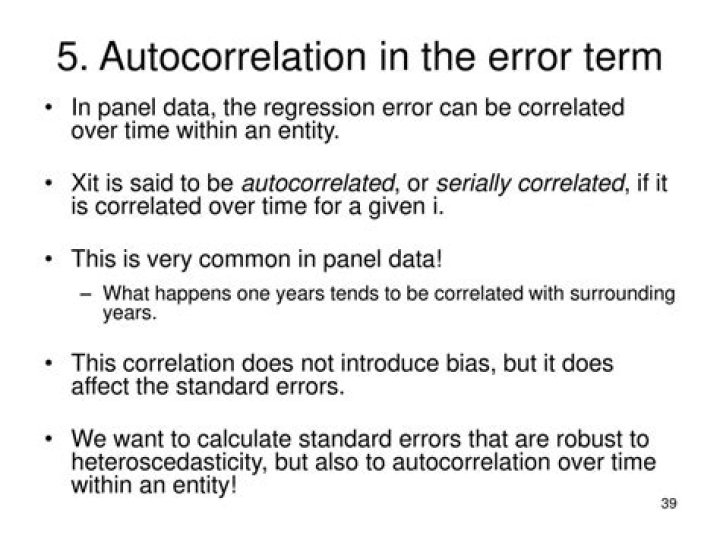

Consequences of Serial Correlation. Serial correlation will not affect the unbiasedness or consistency of OLS estimators, but it does affect their efficiency. With positive serial correlation, the OLS estimates of the standard errors will be smaller than the true standard errors.

What does serially correlated mean?

Serial correlation is the relationship between a given variable and a lagged version of itself over various time intervals. It measures the relationship between a variable’s current value given its past values. A variable that is serially correlated indicates that it may not be random.

How does autocorrelation affect standard errors?

From the Wikipedia article on autocorrelation: While it does not bias the OLS coefficient estimates, the standard errors tend to be underestimated (and the t-scores overestimated) when the autocorrelations of the errors at low lags are positive.

Why is stationarity important for OLS estimation?

A stationarity test of the variables is required because Granger and Newbold (1974) found that regression models for non-stationary variables give spurious results. Thus, the positive relationship between the two series estimated by a regression model may be spurious.

Is serial correlation bad?

Violations of independence are also very serious in time series regression models: serial correlation in the residuals means that there is room for improvement in the model, and extreme serial correlation is often a symptom of a badly mis-specified model, as we saw in the auto sales example.

Why is autocorrelation a problem in regression?

In the classical linear regression model we assume that successive values of the disturbance term are temporarily independent when observations are taken over time. But when this assumption is violated then the problem is known as Autocorrelation.

Does correlation cause Heteroskedasticity?

if there is serial correlation, you’re assuming weak stationarity, and so heteroskedasticity is impossible.

Is stationary required for linear regression?

1 Answer. What you assume in a linear regression model is that the error term is a white noise process and, therefore, it must be stationary. It’s possible for it to be stationary, as in a cointegration model for example, but it need not be.

Does regression require stationary data?

For regression analysis to be performed, data has to be stationary. Or the equation has to be rewritten in such a form that indicates a relationship among stationary variables.

How does serial correlation affect OLS estimators?

, errors in one time period are positively correlated with errors in the next time period. Consequences of Serial Correlation. Serial correlation will not affect the unbiasedness or consistency of OLS estimators, but it does affect their efficiency. With positive serial correlation, the OLS estimates of the standard errors will be.

What is serial correlation?

What Serial Correlation is. When error terms from different (usually adjacent) time periods (or cross-section observations) are correlated, we say that the error term is.

What iscorrelation in time series research?

correlation occurs in time-series studies when the errors associated with a given time period carry over into future time periods. For example, if we are prediciting the growth of stock dividends, an overestimate in one year is likely to lead to overestimates in succeeding years. There are different types of serial correlation.

What is the relationship between errors in one time period and time?

, errors in one time period are correlated directly with errors in the ensuing time period. (Errors might also be lagged, e.g. if data are collected quarterly, the errors in Fall of one year might be correlated with the errors of Fall in the next year.) With positive serial correlation