What does D stand for in Black-Scholes?

Robert Miller

Published Feb 18, 2026

What does D stand for in Black-Scholes?

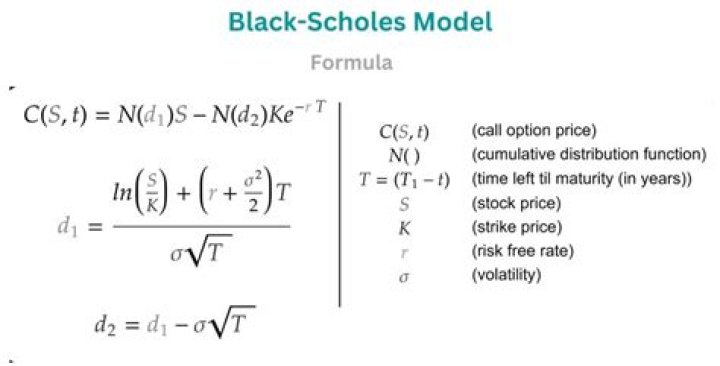

d1 = (ln(S0/K) + (r + σ2/2)T)/(σ√T) N(d1) = a statistical measure (normal distribution) corresponding to the call option’s delta. d2 = d1 – (σ√T) N(d2) = a statistical measure (normal distribution) corresponding to the probability that the call option will be exercised at expiration.

Is Delta equal to n d1?

By definition, we immediately have N(d1) as the option delta, representing the changing rate of the option price as a result of the stock price change. It can be further shown that N(d2) actually is the probability the option will be exercised.

What is the difference between n d1 and n D2?

D2 is the probability that the option will expire in the money i.e. spot above strike for a call. N(D2) gives the expected value (i.e. probability adjusted value) of having to pay out the strike price for a call. D1 is a conditional probability. A gain for the call buyer occurs on two factors occurring at maturity.

What does nd1 and nd2 represent in Black-Scholes?

In linking it with the contingent receipt of stock in the Black Scholes equation, N(d1) accounts for: the probability of exercise as given by N(d2), and. the fact that exercise or rather receipt of stock on exercise is dependent on the conditional future values that the stock price takes on the expiry date.

What is volatility in Black Scholes model?

Implied volatility is an estimate of the future variability for the asset underlying the options contract. The inputs for the Black-Scholes equation are volatility, the price of the underlying asset, the strike price of the option, the time until expiration of the option, and the risk-free interest rate.

What is C in Black-Scholes?

The Black-Scholes formula for the value of a call option C for a non-dividend paying stock of price S. The formula gives the value/price of European call options for a non-dividend-paying stock.

How do you interpret N d1 in Black Scholes?

So, N(d1) is the factor by which the discounted expected value of contingent receipt of the stock exceeds the current value of the stock. By putting together the values of the two components of the option payoff, we get the Black-Scholes formula: C = SN(d1) − e−rτ XN(d2).

What is d1 in the Black Scholes model?

What is the Black Scholes model?

The Black Scholes model is a mathematical model that models financial markets containing derivatives. The Black Scholes model contains the Black Scholes equation which can be used to derive the Black Scholes formula. The Black Scholes formula can be used to model options prices and it is this formula that will be the main focus of this article.

What are the parameters of the Black-Scholes formula?

The Black–Scholes formula has only one parameter that cannot be directly observed in the market: the average future volatility of the underlying asset, though it can be found from the price of other options.

How is a European call valued using the Black–Scholes pricing equation?

A European call valued using the Black–Scholes pricing equation for varying asset price S {displaystyle S} and time-to-expiry T {displaystyle T} . In this particular example, the strike price is set to 1. The Black–Scholes formula calculates the price of European put and call options.

How do you find the price at expiration in Black Scholes?

In the Black Scholes formula notation, this would be: Intrinsic value = S – K This is exactly what you get when you plug in 0 for T which would be the option’s price at expiration in the Black Scholes formula. In other words, at expiration, an option will only have extrinsic value left.