What do underwriters look for in a conventional loan?

Michael Henderson

Published Feb 08, 2026

What do underwriters look for in a conventional loan?

Capacity. When trying to determine whether you have the means to pay off the loan, the underwriter will review your employment, income, debt and assets. They’ll look at your savings, checking, 401k and IRA accounts, tax returns and other records of income, as well as your debt-to-income ratio.

Why would an underwriter deny a conventional loan?

Whether in the beginning or end, reasons for a mortgage loan denial may include credit score drop, property issues, fraud, job loss or change, undisclosed debt, and more.

How often do underwriters deny conventional loans?

One in every 10 applications to buy a new house — and a quarter of refinancing applications — get denied, according to 2018 data from the Consumer Financial Protection Bureau. Rather than focusing on the rejection, try to chart your next steps.

What are the 4 C’s of mortgage underwriting?

Standards may differ from lender to lender, but there are four core components — the four C’s — that lender will evaluate in determining whether they will make a loan: capacity, capital, collateral and credit.

What is frontline underwriting?

Frontline underwriting of mortgage loans (retail, wholesale, jumbo, correspondent) on both a delegated and non-delegated basis. Interpret credit policy guidelines and investor guidelines and apply them to specific loans for effective sale in the secondary market.

How long does it take for the underwriter to make a decision?

Under normal circumstances, initial underwriting approval happens within 72 hours of submitting your full loan file. In extreme scenarios, this process could take as long as a month. However, it’s unlikely to take so long unless you have an exceptionally complicated loan file.

Do conventional loans go through underwriting?

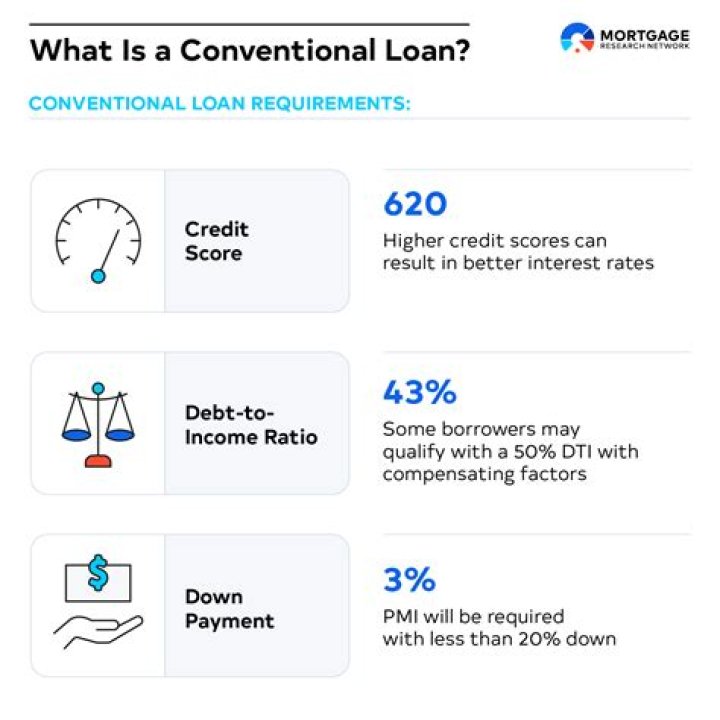

Your credit score should be at least 620 if you apply for a conventional loan. Your underwriter will also pull your credit report and look at your payment history, your credit usage and the age of your accounts. The underwriter looks at your credit report to determine your debt-to-income (DTI) ratio.

What does PMI stand for?

Private mortgage insurance

Private mortgage insurance (PMI) is a type of insurance that may be required by your mortgage lender if your down payment is less than 20 percent of your home’s purchase price. PMI protects the lender against losses if you default on your mortgage.

What is the maximum mortgage payment PITI a lender would allow for a conventional loan based on the housing expense ratio?

Lenders also consider a borrower’s income and debt-to-income (DTI) ratio. This means that household expense payments, primarily rent or mortgage payments, can be no more than 28% of the monthly or annual income.

What are the requirements for a conventional mortgage loan?

Conventional loan guidelines require borrowers to have a minimum middle FICO score of 620-680 for approval. Applicants must have made all housing payments on time for at least 12 months. Conventional mortgage requirements contain significant waiting periods after a bankruptcy or foreclosure.

What is a conventional loan and how does it work?

Conventional loans are the go-to financing for most home purchases and refinances, but the demand for conventional mortgages ebbs and flows based on housing market and economic changes.

What is a FHA loan vs conventional?

An FHA loan is easier to acquire for those with low credit scores and requires as little as 3.5% for down payment. The disadvantage of an FHA loan is expensive mortgage insurance, which is paid upfront as well as in monthly installments. Conventional loans are cheaper overall but require good credit.

What is a down payment for a conventional loan?

Conventional home mortgages require down payments of anywhere from 3 to 20 percent of the purchase price. The minimum down payment requirement is contingent on the home loan amount and the homebuyer ‘s credit score and income.