What are the risks of securities lending?

John Castro

Published Mar 18, 2026

What are the risks of securities lending?

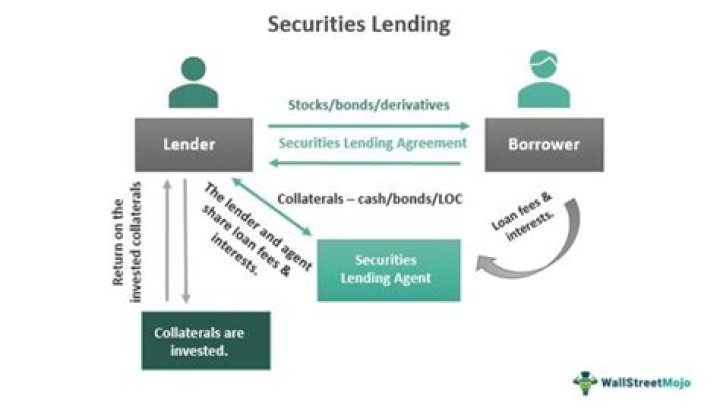

There are two primary risks of securities lending: borrower default risk and cash collateral reinvestment risk. Borrower default risk is the risk that the counterparty fails to return the borrowed security back to the lender.

How do you mitigate a high concentration risk?

The following tips can help manage concentration risk:

- 1 Diversify across, and within, the major asset classes and fund managers/issuers.

- 2 Review regularly and rebalance when needed.

- 3 Look “under the hood” of each investment you own.

- 4 Know how easily you can sell your investments.

What is loan concentration risk?

Credit concentration risk occurs when loans are susceptible to a specific sector of the economy or business group that has slowed down, which is particularly risky for banks and financial institutions.

Why is credit concentration risk important?

The potential importance of concentration risk in actual bank portfolios highlights the need for supervisors to assess the potential gap between Pillar 1 capital requirements and the “true” underlying risk.

Why is stock lending bad?

You’d think the biggest risk in securities lending is that the short-seller you lent shares to goes bankrupt. Fortunately, industry practice is for borrowers to provide collateral exceeding the value of the loaned securities by a set margin. So while a busted counterparty is a pain, it’s not immediately costly.

How do lending stocks make money?

Lending shares is passive and produces more income. WHEN INVESTORS LEND their shares to a broker, they can receive more income over time. Loaning a stock or another asset such as an exchange-traded fund to a brokerage firm can yield investors more income passively.

What type of risk is concentration risk?

Concentration risk was originally a term that banks used to describe credit risk in the form of lending too much to one particular customer or type of customer such as companies in a particular industry. In recent years, the term is also used to describe broader portfolio diversification risks.

What is concentration risk in stock market?

One of the primary purposes of investing is to achieve diversification. It is considered to be a measure of risk mitigation. Essentially, concentration risk is the risk that your portfolio returns may be imperilled because there is too much dependency on a set of factors or triggers.

What is the purpose of a concentration limit?

A concentration limit limits the amount of exposure a lender has to a single debtor on your ledger. Typically, concentration limits will not be an issue for many businesses who have a good spread of customers.

What is a concentration limit?

A concentration limit is the percentage of a borrower’s total receivables portfolio that can come from one customer category while still getting “full credit” from a lender. Common examples of concentration limits include the percentage of a portfolio that comes from a single customer, geography, or industry.

Do you consider concentration in banking positive?

Concentration as a Benefit (cont) High concentration levels will increase profits for the dominant banks within the industry. While this may lead to higher interest rates and fees it will also insulate banks from economic shocks.

Is securities lending a good idea?

Generally speaking, securities-lending activities are positives for shareholders and contribute to tighter index tracking and better overall returns. They are not without some risks; while we believe they are generally minor, they are nonetheless worth considering.

What are the risks involved in securities lending?

In spite of strict standards of collateralization, securities lending activities involve risk of loss. Such risks may arise from malfeasance or failure of the borrowing firm or institution. Therefore, a duly established management or supervisory committee of the lender institution should formally approve, in advance, transactions with any borrower.

What happens when a loan becomes over-collateralized?

If a loan becomes over-collateralized because of appreciation of collateral or market depreciation of a loaned security, the borrower usually has the opportunity to request the return of any excessive margin. When a securities loan is terminated, the securities are returned to the lender and the collateral to the borrower.

What are credit limits and concentration limits?

Credit and concentration limits should take into account other extensions of credit by the lender institution to the same borrower or related interests.

Who is the finder of Securities and collateral?

Securities and collateral are delivered directly by the borrower and the lender without the involvement of the finder. The finder is simply a fully disclosed intermediary. All financial institutions that participate in securities lending should establish written policies and procedures governing these activities.