What are the respa disclosures

Emma Martin

Published Apr 16, 2026

RESPA requires that borrowers receive disclosures at various times in the transaction process. Some disclosures spell out the costs associated with the settlement, outline lender servicing and escrow account practices and describe business relationships between settlement service providers.

What disclosures are required by RESPA?

One requirement of RESPA is that disclosures are provided to borrowers at various times throughout the settlement process. These disclosures include information regarding costs, lender servicing, escrow account practices, and business relationships between settlement providers.

What are the two types of disclosures required to provide to borrowers?

Those include the special information booklet for homebuyers, the Good Faith Estimate for all applicants, and the Mortgage Servicing Disclosure for all applicants.

What are the 6 pieces of RESPA?

- The consumer’s name;

- The consumer’s income;

- The consumer’s social security number to obtain a credit report;

- The property address;

- An estimate of the value of the property; and.

Which disclosures are required by RESPA for Trid loans?

When you’re looking for a mortgage, TRID guidelines dictate that your mortgage lender must provide you with two unique disclosures: the Loan Estimate and the Closing Disclosure.

What disclosures are required for a mortgage loan?

Loan Application When you apply for a mortgage, the lender or the mortgage broker must give you several disclosures, including a good faith estimate, a mortgage servicing disclosure statement, and a consumer information booklet. The good faith estimate spells out the estimated fees you’ll need to pay at closing.

What is exempt from RESPA?

The following transactions are exempt from RESPA: • A loan on property of twenty-five acres or more. (whether or not a dwelling is located on the. property) • A loan primarily for business, commercial, or.

What is the 3 day Trid rule?

Quick Review of the Three Day Closing Disclosure Rule The federal law that regulates the mortgage process (known as the TRID) requires that lenders provide borrowers with a closing disclosure at least three business days before the close of the mortgage.What does PITI stand for?

PITI is an acronym that stands for principal, interest, taxes and insurance. Many mortgage lenders estimate PITI for you before they decide whether you qualify for a mortgage.

What is the 3 7 3 rule in mortgage terms?The 3/7/3 Rule requires a seven business day waiting period once the initial disclosure is provided before closing a home loan (business days are everyday except Sundays and Holidays).

Article first time published onWhat are the two types of disclosures?

The two new forms, the Loan Estimate and the Closing Disclosure, combine information and mirror each other, so you can easily compare the terms you were given on the Loan Estimate with the terms on the Closing Disclosure.

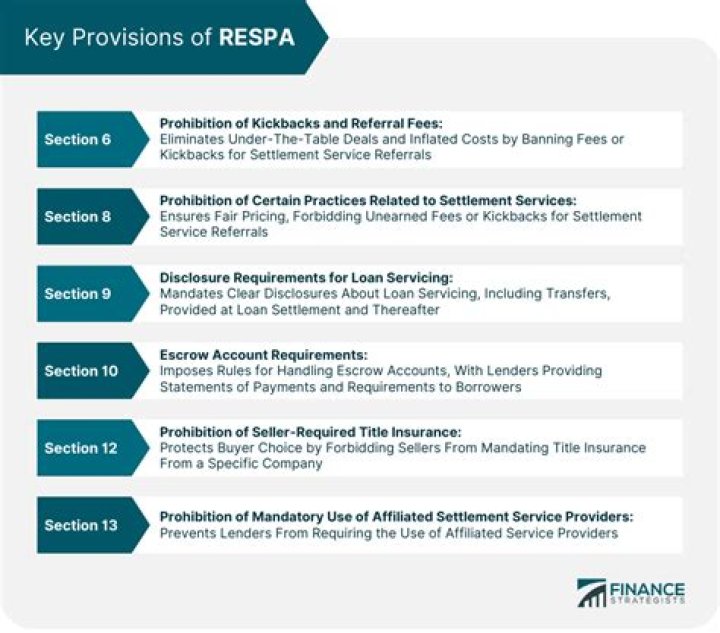

What are RESPA rules?

RESPA prohibits loan servicers from demanding excessively large escrow accounts and restricts sellers from mandating title insurance companies. A plaintiff has up to one year to bring a lawsuit to enforce violations where kickbacks or other improper behavior occurred during the settlement process.

Which of the following is a disclosure that must be provided before settlement?

Disclosures Before Settlement Before settlement, the lender must provide the borrower with an Affiliated Business Arrangement Disclosure when the settlement provider refers the borrower to another settlement provider with whom the referring party has some form of ownership interest.

How many closing disclosures are there?

There will be two Closing Disclosures issued during the process: the “Initial CD” and the “Final CD”. The Initial CD is the most time-sensitive document throughout the mortgage loan process because it requires e-signatures a minimum of three days before closing.

How do the TILA-respa integrated disclosures help the consumer?

TRID provides consumers with a clearer easier to understand estimate of the costs involved in a mortgage. Providing consumers a more convenient way of comparing loan offers from mortgage lenders. TRID reduces the amount of paperwork required and provides a more transparent and accurate loan estimate.

Does respa apply to HELOCs?

The TILA-RESPA rule applies to most closed-end consumer credit transactions secured by real property, but does not apply to: HELOCs; • Reverse mortgages; or • Chattel-dwelling loans, such as loans secured by a mobile home or by a dwelling that is not attached to real property (i.e., land).

Are bridge loans subject to RESPA?

A “bridge loan” or “swing loan” in which a lender takes a security interest in otherwise covered 1- to 4-family residential property is not covered by RESPA and this part.

What is a referral under RESPA?

As discussed in RESPA Section 8(a) FAQ 1, referrals include any oral or written action directed to a person where the action has the effect of affirmatively influencing the selection of a particular provider of settlement services or business incident thereto by a person paying a charge attributable to the service or …

What are kickbacks in real estate?

Real estate agent kickbacks are an under the table exchange of cash or goods to incentivize real estate agents to send business to services. It’s important to distinguish real estate agent kickbacks from finders fees or referral fees. One of these is illegal.

What is respa in mortgage?

The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. … The act requires lenders, mortgage brokers, or servicers of home loans to provide borrowers with pertinent and timely disclosures regarding the nature and costs of the real estate settlement process.

What are initial disclosures mortgage?

Initial disclosures are the preliminary disclosures that must be acknowledged and signed in order to move forward with your loan application. … Initial disclosures let you know what you can expect in terms of cost, monthly payments, and loan structure.

What are disclosures in the loan process?

The Closing Disclosure is a five-page form that describes, in detail, the critical aspects of your mortgage loan, including purchase price, loan fees, interest rate, estimated real estate taxes and insurance, closing costs and other expenses.

What does PMI stand for?

Private mortgage insurance (PMI) is a type of insurance that may be required by your mortgage lender if your down payment is less than 20 percent of your home’s purchase price. PMI protects the lender against losses if you default on your mortgage.

What are the 4 Cs of credit?

Standards may differ from lender to lender, but there are four core components — the four C’s — that lender will evaluate in determining whether they will make a loan: capacity, capital, collateral and credit.

What is monthly P and I?

Your monthly mortgage payment can be broken down into four parts: principal, interest, taxes, and insurance. Together, these parts are known as “PITI.”

Do Saturdays count for Trid?

When it comes to disclosures to meet TRID guidelines, Saturday counts as a business day. … Basically, a lender must provide a borrower with a closing disclosure at least three business days before they sign their loan. Oddly, business days are not defined by business hours. Two business days are not 48 hours.

Can buyer waive 3 day closing disclosure?

A consumer may modify or waive the right to the three-day waiting period only after receiving the disclosures required by § 1026.32 and only if the circumstances meet the criteria for establishing a bona fide personal financial emergency under § 1026.23(e).

Do Saturdays count for loan estimates?

General business days do not include Saturdays unless the lender is normally open on Saturday to conduct substantially all of its business. If the lender is normally open on Saturdays then they must include Saturday when counting the 3 days for the required mailing/delivery of the Loan Estimate.

What is Regulation Z?

Regulation Z is a law that protects consumers from predatory lending practices. Also known as the Truth in Lending Act, the law requires lenders to disclose borrowing costs so consumers can make informed choices.

What are the 6 Trid triggers?

The six items are the consumer’s name, income and social security number (to obtain a credit report), the property’s address, an estimate of property’s value and the loan amount sought.

How many days after the loan estimate can you close?

DocumentWhen you get itWhen it showsLoan estimateWithin 3 business days after applying for a loanEstimated loan terms and costsClosing disclosureAt least 3 business days before closing your loanFinal loan terms and costs