Is bivariate normal independent?

Sarah Cherry

Published Mar 15, 2026

Is bivariate normal independent?

In the case of jointly normal random variables, the converse is true. Thus, for jointly normal random variables, being independent and being uncorrelated are equivalent. If X and Y are bivariate normal and uncorrelated, then they are independent.

How do you know if a conditional distribution is independent?

If X and Y are independent, the conditional pdf of Y given X = x is f(y|x) = f(x, y) fX(x) = fX(x)fY (y) fX(x) = fY (y) regardless of the value of x.

How do you know if a bivariate random variable is independent?

Recall that events A and B are independent if and only if P[A and B] = P[A] P[B]. For discrete random variables, the condition for independence of X and Y becomes X and Y are independent if and only if P[X=x,Y=y] = P[X=x] P[Y=y] for all real numbers x and y.

Is bivariate normal symmetric?

This tells us something useful about this special case of the bivariate normal distributions: it is rotationally symmetric about the origin. This particular fact is incredibly powerful and helps us solve a variety of problems.

What is the primary purpose of the bivariate distribution?

The primary purpose of bivariate data is to compare the two sets of data to find a relationship between the two variables. Remember, if one variable influences the change in another variable, then you have an independent and dependent variable.

How can you tell if joint pdf is independent?

Independence: X and Y are called independent if the joint p.d.f. is the product of the individual p.d.f.’s, i.e., if f(x, y) = fX(x)fY (y) for all x, y.

How do you find conditional expectation from a joint distribution?

yg(x)pX,Y (x, y) = E[Y g(X)]. Exercise: Prove E[Y g(X)] = E[E[Y |X]g(X)] if X and Y are jointly continuous random variables. The conditional expectation E[Y |X] can be viewed as an estimator of Y given X. Y − E(Y |X) is then the estimation error for this estimator.

What is a bivariate expectation?

If your random variable is bivariate, then every realization is a pair of numbers. The expectation of a random number can be thought of as “the long-run average”. A long-run average of a large number of pairs makes most sense as a pair of numbers, not a single number.

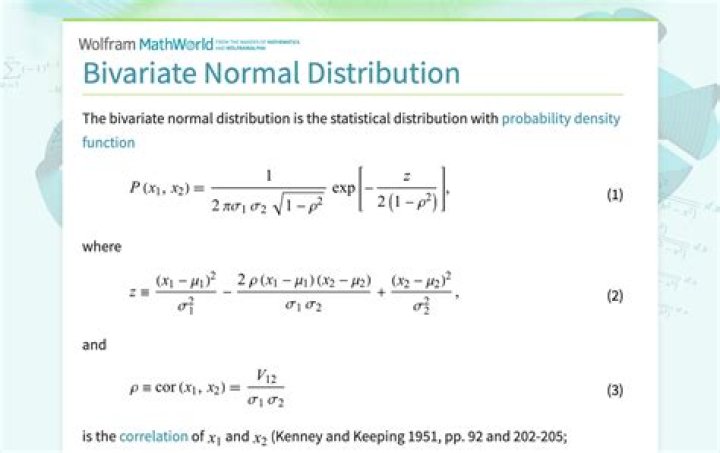

What is bivariate normality?

What is a Bivariate Normal Distribution? The “regular” normal distribution has one random variable; A bivariate normal distribution is made up of two independent random variables. The two variables in a bivariate normal are both are normally distributed, and they have a normal distribution when both are added together.

Which distribution is bivariate?

The “regular” normal distribution has one random variable; A bivariate normal distribution is made up of two independent random variables. The two variables in a bivariate normal are both are normally distributed, and they have a normal distribution when both are added together.

How do you sample a bivariate normal distribution?

Hence, a sample from a bivariate Normal distribution can be simulated by first simulating a point from the marginal distribution of one of the random variables and then simulating from the second random variable conditioned on the first. A brief proof of the underlying theorem is available here.