How long does refinance approval take

Robert Miller

Published Apr 14, 2026

Refinances can take from about 45 to 60 days depending on several factors, including the type of loan.

Why is my refi taking so long?

Are you wondering why does it take so long to refinance a mortgage? The simple answer is because lending standards have tightened tremendously since the 2008-2009 Global Financial Crisis. Underwriters are asking for more documentation to prove your income and net worth.

Can you get denied for a refinance?

Why Lenders Reject Refinance Applications A lender may reject a home refinance application for a multitude of reasons. Chief among them: Weak credit score and credit history: Lenders don’t like to see late payments and collection accounts on a credit report, since they may be indicators of financial irresponsibility.

Is it hard to get approved for refinance?

If your score is below the mid-600s, you may have a hard time qualifying for a refinance. To be approved for a conventional mortgage, you typically need a credit score of 620 or higher. … For example, a history of late mortgage payments can hurt your chances at a refinance no matter what your score is.How long does a refinance take in 2020?

As mentioned, a typical refinance can take 30 to 45 days to close. It took about 50 days, on average, to close a refinance for all loan types as of August 2020, according to the latest Ellie Mae Origination Insight Report.

How fast can a refinance close?

You can refinance your mortgage loan to take advantage of lower interest rates, change your term, consolidate debt or take cash out of your equity. Though there is no exact time limit on how long a refinance can take, most refinances close within 30 to 45 days of your application.

How long does the underwriting process take for a refinance?

Underwriting can take anywhere from a couple of days to several weeks, but the average is a week or two. Your lender will issue your approval once underwriting is complete.

How much income do I need to refinance?

And there may even be more wiggle room than that: Denny Ceizyk, senior staff writer for LendingTree, says lenders typically use a maximum debt-to-income ratio of 43% of your pre-tax income to qualify you for a refinance.Is refinancing harder than getting a mortgage?

For Lower-Credit Homeowners, Refinancing Is Harder, but Not Hopeless. … With mortgage interest rates hitting record lows, many homeowners have already refinanced — but others are having trouble finding a lender that will approve a new loan.

What credit score do I need to refinance my house?Credit requirements vary by lender and type of mortgage. In general, you’ll need a credit score of 620 or higher for a conventional mortgage refinance. Certain government programs require a credit score of 580, however, or have no minimum at all.

Article first time published onHow much debt can you have to refinance?

DTI ratio: Your DTI ratio is the total amount of your monthly debt payments divided by your gross monthly income. This is what lenders look at when deciding if you’ll be able to afford your mortgage payments. In most cases, the highest DTI you can have to get approved for mortgage refinancing is 43%.

Can I refinance my house with a 600 credit score?

The cut-off to qualify for a conventional fixed-rate home loan is roughly a 620 credit score. The cut-off for a Federal Housing Administration (FHA)-backed mortgage is as low as 580. The cut-off for refinancing is about 620—really considered a poor score and not bad, which is 600 or less.

Does debt-to-income ratio affect refinance?

Simply put, it is the percentage of your monthly pre-tax income you must spend on your monthly debt payments plus the projected payment on the new home loan. Generally, the lower your debt-to-income ratio is, the more likely you are to qualify for a mortgage.

Does refinancing hurt credit?

Taking on new debt typically causes your credit score to dip, but because refinancing replaces an existing loan with another of roughly the same amount, its impact on your credit score is minimal.

How long does a streamline refinance take?

In an ideal situation, a borrower can expect a streamline refinance to be completed anywhere from 30 days to as little as a few weeks. The typical refinance loan process can take 45 to 60 days.

What happens after closing on a refinance?

At closing, you’ll go over the details of the loan and sign your loan documents. This is when you’ll pay any closing costs that aren’t rolled into your loan. If your lender owes you money (for example, if you’re doing a cash-out refinance), you’ll receive the funds after closing.

How do you know when your mortgage loan is approved?

How do you know when your mortgage loan is approved? Typically, your loan officer will call or email you once your loan is approved. Sometimes, your loan processor will pass along the good news.

Is no news good news when loan is in underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

Do underwriters look at spending habits?

Banks check your credit report for outstanding debts, including loans and credit cards and tally up the monthly payments. … Bank underwriters check these monthly expenses and draw conclusions about your spending habits.

How long is an appraisal good for refinancing?

Generally, a home appraisal is good for a total of 120 days (4 months). If you do not close on your home within that time, you will need to have another assessment. Some people may be afforded an extension, but only in certain circumstances and only if they’re eligible.

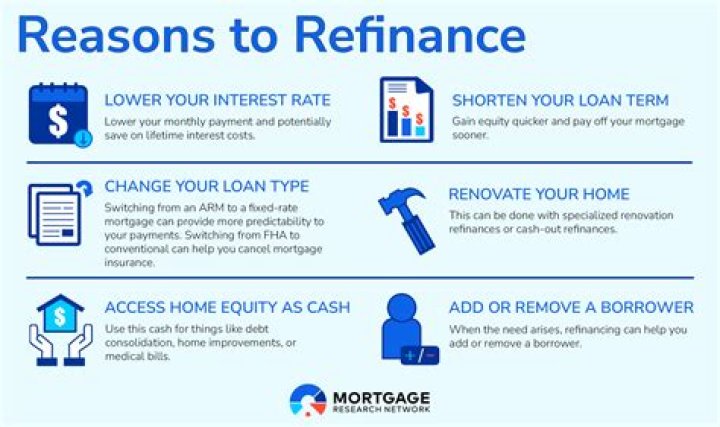

Does refinancing lower interest rate?

Refinancing can lower your monthly mortgage payment by reducing your interest rate or increasing your loan term. Refinancing also can lower your long-run interest costs through a lower mortgage rate, shorter loan term or both.

Can I refinance twice in a year?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do have a few mortgage refinance requirements that need to be met each time you apply, and there are some special considerations to note if you want a cash-out refinance.

How do you know if refinance is worth it?

Mortgage rates have gone down So how much should mortgage rates fall before you consider whether refinancing is worth it? The traditional rule of thumb says to refinance if your rate is 1% to 2% below your current rate. Make sure to factor in your current loan term when considering refinance though.

Should I refinance if I only have 5 years left?

It’s usually better to refinance when: The upfront costs of refinancing pay off when you stay in the home long enough to benefit from the new loan’s savings. You’re not far into the existing loan. If you’ve only had your existing mortgage a few years, you’re more likely to save money in the long run by refinancing.

What percentage difference Should you refinance?

The traditional rule of thumb is that it makes financial sense to refinance if the new rate is 2 percent or more below your existing interest rate. The new rate on a refinance must provide enough savings in monthly mortgage payment to justify the cost of refinancing.

How much do I need to make for a 250k mortgage?

How Much Income Do I Need for a 250k Mortgage? You need to make $76,906 a year to afford a 250k mortgage. We base the income you need on a 250k mortgage on a payment that is 24% of your monthly income. In your case, your monthly income should be about $6,409.

What percentage of home value can you refinance?

The 20 Percent Equity Rule When it comes to refinancing, a general rule of thumb is that you should have at least a 20 percent equity in the property. However, if your equity is less than 20 percent, and if you have a good credit rating, you may be able to refinance anyway.

How many times is your credit pulled when refinancing?

While the number of credit checks for a mortgage can vary depending on the situation, most lenders will check your credit up to three times during the application process.

Can you refinance if you are in forbearance?

Borrowers can refinance after a forbearance, but only if they make timely mortgage payments following the forbearance period. If you have ended your forbearance and made the required number of on-time payments, you can start the refinancing process.

What's a good FICO score?

Although ranges vary depending on the credit scoring model, generally credit scores from 580 to 669 are considered fair; 670 to 739 are considered good; 740 to 799 are considered very good; and 800 and up are considered excellent.

Can you refinance after forbearance?

And you’re probably wondering what comes next. With mortgage rates near record lows, you may want to refinance. This could reduce your monthly payments and make your home loan more affordable. The good news is, refinancing after forbearance is generally allowed.