How is monthly mortgage calculated

Sarah Cherry

Published Apr 13, 2026

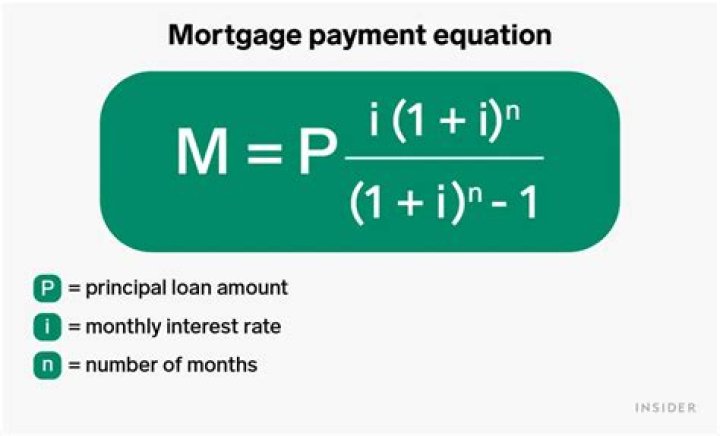

If you want to do the monthly mortgage payment calculation by hand, you’ll need the monthly interest rate — just divide the annual interest rate by 12 (the number of months in a year). For example, if the annual interest rate is 4%, the monthly interest rate would be 0.33% (0.04/12 = 0.0033).

What is the formula for calculating monthly mortgage payment?

If you want to do the monthly mortgage payment calculation by hand, you’ll need the monthly interest rate — just divide the annual interest rate by 12 (the number of months in a year). For example, if the annual interest rate is 4%, the monthly interest rate would be 0.33% (0.04/12 = 0.0033).

What is monthly mortgage based on?

Your monthly mortgage payment will depend on your home price, down payment, loan term, property taxes, homeowners insurance, and interest rate on the loan (which is highly dependent on your credit score).

What is the formula for calculating a 30 year mortgage?

Multiply the number of years in your loan term by 12 (the number of months in a year) to get the number of total payments for your loan. For example, a 30-year fixed mortgage would have 360 payments (30×12=360).How do you calculate monthly payments?

- a: $100,000, the amount of the loan.

- r: 0.005 (6% annual rate—expressed as 0.06—divided by 12 monthly payments per year)

- n: 360 (12 monthly payments per year times 30 years)

Is mortgage interest calculated monthly or daily?

The standard mortgage in the US accrues interest monthly, meaning that the amount due the lender is calculated a month at a time. There are some mortgages, however, on which interest accrues daily.

How is interest calculated monthly?

To calculate the monthly interest, simply divide the annual interest rate by 12 months. The resulting monthly interest rate is 0.417%. The total number of periods is calculated by multiplying the number of years by 12 months since the interest is compounding at a monthly rate.

How do you calculate monthly amortization?

To calculate amortization, start by dividing the loan’s interest rate by 12 to find the monthly interest rate. Then, multiply the monthly interest rate by the principal amount to find the first month’s interest. Next, subtract the first month’s interest from the monthly payment to find the principal payment amount.How do I calculate monthly mortgage payment in Excel?

Calculate the monthly payment. To figure out how much you must pay on the mortgage each month, use the following formula: “= -PMT(Interest Rate/Payments per Year,Total Number of Payments,Loan Amount,0)“. For the provided screenshot, the formula is “-PMT(B6/B8,B9,B5,0)”.

How can I pay off my mortgage in 5 years?- Create A Monthly Budget. …

- Purchase A Home You Can Afford. …

- Put Down A Large Down Payment. …

- Downsize To A Smaller Home. …

- Pay Off Your Other Debts First. …

- Live Off Less Than You Make (live on 50% of income) …

- Decide If A Refinance Is Right For You.

What is the 28 36 rule?

A Critical Number For Homebuyers One way to decide how much of your income should go toward your mortgage is to use the 28/36 rule. According to this rule, your mortgage payment shouldn’t be more than 28% of your monthly pre-tax income and 36% of your total debt. This is also known as the debt-to-income (DTI) ratio.

Do you have until the 15th to pay mortgage?

So even though your mortgage payments are technically due on the first each month, you can pay as late as the 15th every month without any kind of penalty. … This is known as the “mortgage grace period,” similar to other grace periods you see with all types of other loans.

How much of my monthly income should I spend on a mortgage?

The 28% rule states that you should spend 28% or less of your monthly gross income on your mortgage payment (e.g. principal, interest, taxes and insurance). … Using these figures, your monthly mortgage payment should be no more than $2,800.

What is the formula of loan calculation?

Great question, the formula loan calculators use is I = P * r *T in layman’s terms Interest equals the principal amount multiplied by your interest rate times the amount in years.

How much income do I need for a 200k mortgage?

A $200k mortgage with a 4.5% interest rate over 30 years and a $10k down-payment will require an annual income of $54,729 to qualify for the loan. You can calculate for even more variations in these parameters with our Mortgage Required Income Calculator.

What is the monthly payment on $10000?

Your payments on a $10,000 personal loanMonthly payments$201$379Interest paid$2,060$12,712

How do you calculate monthly APR?

- Step 1: Find your current APR and current balance in your credit card statement.

- Step 2: Divide your current APR by 12 (for the twelve months of the year) to find your monthly periodic rate.

- Step 3: Multiply that number with the amount of your current balance.

What is the monthly interest rate?

A monthly interest rate is simply how much interest you would be charged in one month. This doesn’t include any other charges associated with the loan, and it doesn’t show exactly how expensive a loan actually is. APR, on the other hand, is the percentage rate charged on a loan over the term of one year.

How do you calculate principal and interest payments?

In order to determine what proportion of this payment is interest and principal, do the following. First, convert your annual interest rate from a percentage into a decimal format by diving the figure by 100. So, 5/ 100 = 0.05. Next, divide this number by 12 to compute your monthly interest rate.

What APR means on mortgage?

APR is the annual cost of a loan to a borrower — including fees. Like an interest rate, the APR is expressed as a percentage. Unlike an interest rate, however, it includes other charges or fees such as mortgage insurance, most closing costs, discount points and loan origination fees.

Is it better to have interest compounded daily or monthly?

Between compounding interest on a daily or monthly basis, daily compounding gives a higher yield – although the difference could be small. … When you look to open a savings account or something similar like CDs, you quickly learn that not every bank offers the same interest rate.

Do you pay less interest if you pay weekly?

If you pay your mortgage repayments weekly or fortnightly, you are paying down the principal amount faster, and thus reducing the interest that will accumulate. Interest is calculated on the principal balance, so with less principal owing, there’s less interest payable.

How do I calculate mortgage payments in Excel?

Enter the formula “=B3” in cell E2 (the first month of your mortgage) in the balance column. Type the formula “=$B$9” in cell F2, the payment column. Enter “=E2-F2” in cell G2, the remaining column. Type “=G2*$B$7” in cell H2 for the interest calculation.

What is a good amortization period?

The most common amortization is 25 years. If you have at least a 20% down payment, however, you can go higher—up to 30 years, and sometimes longer. Shorter amortizations are also available. Their benefit is helping you accumulate home equity faster.

When loans are amortized monthly payments are?

An amortizing loan is a type of debt that requires regular monthly payments. Each month, a portion of the payment goes toward the loan’s principal and part of it goes toward interest. Also known as an installment loan, fully amortized loans have equal monthly payments.

What does a 15 year amortization mean?

Fixed-Rate Mortgages A fixed-rate mortgage fully amortizes at the end of the term. In the case of a 15-year fixed-rate mortgage, the loan is paid in full at the end of 15 years. … Loans with shorter terms have less interest because they amortize over a shorter period of time.

Should I aggressively pay off my mortgage?

It’s often more beneficial for newer owners to be aggressive with their mortgage payments. This is because your money is typically going towards the interest on the loan, not the principal itself. This means that any extra payments will reduce the total amount of interest owed over the course of the entire loan.

What to do after house is paid off?

- Get a Satisfaction of Mortgage Statement. …

- File the Satisfaction of Mortgage Statement With your county clerk. …

- Cancel automatic mortgage payments. …

- Notify your homeowner insurance provider. …

- Contact your local taxing authority. …

- Inquire about your escrow balance. …

- Check your credit report.

Is it smart to pay off your house?

Paying off your mortgage early helps you save money in the long run, but it isn’t for everyone. Paying off your mortgage early is a good way to free up monthly cashflow and pay less in interest. But you’ll lose your mortgage interest tax deduction, and you’d probably earn more by investing instead.

What's the 50 30 20 budget rule?

The 50-20-30 rule is a money management technique that divides your paycheck into three categories: 50% for the essentials, 20% for savings and 30% for everything else. 50% for essentials: Rent and other housing costs, groceries, gas, etc.

Is it bad to be house poor?

Becoming house poor can affect your ability to save for retirement, pay off debt or afford other purchases. Experts recommend saving 3 – 6 months’ worth of living expenses for an emergency fund. That’s before considering retirement savings.