How does IFRS 16 affect financial statements?

Robert Miller

Published Mar 19, 2026

How does IFRS 16 affect financial statements?

What is the impact and effect of IFRS 16 on financial statements? The introduction of IFRS 16 / AASB 16 will lead to an increase in leased assets and financial liabilities on the balance sheet of the lessee. Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) of the lessee increases as well.

How does IFRS 16 affect balance sheet?

The introduction of IFRS 16 will lead to an increase in leased assets and financial liabilities on the balance sheet of the lessee, while Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA) of the lessee increases as well.

How does IFRS 16 affect cash flow statement?

Are there any implications for cash flows? Changes in accounting requirements do not change amount of cash transferred between the parties to a lease. Consequently, IFRS 16 will not have any effect on the total amount of cash flows reported.

How do you do closing entries in accounting?

- Step 1: Close all income accounts to Income Summary. Date.

- Step 2: Close all expense accounts to Income Summary. Income Summary.

- Step 3: Close Income Summary to the appropriate capital account. Now for this step, we need to get the balance of the Income Summary account.

- Step 4: Close withdrawals to the capital account.

Do you include service charge in IFRS 16?

IFRS 16 does not change the accounting for services. Although leases and services are often combined in a single contract, amounts related to services are not required to be reported on the balance sheet.

How do you recognize right of use assets IFRS 16?

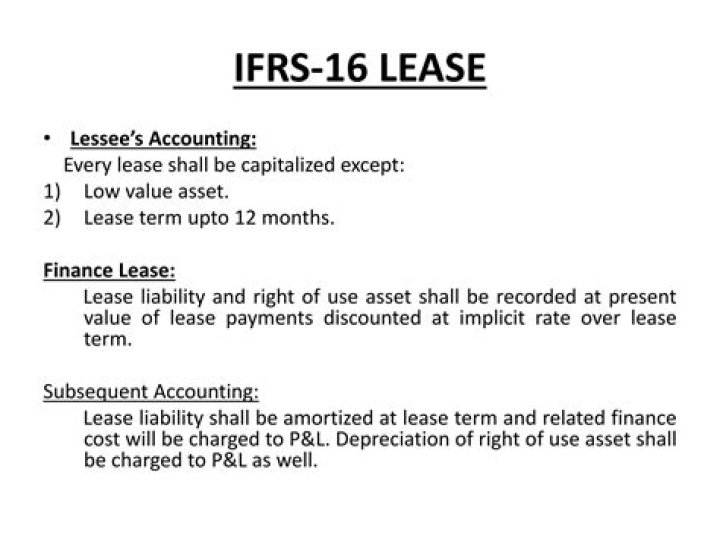

IFRS 16 requires that the ‘right of use asset’ and the lease liability should initially be measured at the present value of the minimum lease payments. The discount rate used to determine present value should be the rate of interest implicit in the lease.

How is IFRS 16 different?

IFRS 16 applies only to leases, or lease components of a contract. IFRS 16 changes significantly how a company accounts for leases that were off balance sheet applying IAS 17, other than short-term leases (leases of 12 months or less) and leases of low-value assets (such as personal computers and office furniture).

Does IFRS 16 affect capex?

Capex and depreciation Prior to IFRS 16, unless a company was forecasted to have significant growth capex, a common assumption used by valuers and analysts was that capex equals depreciation. However, post IFRS 16 this simplifying assumption will no longer be valid.

What are the 4 steps in the closing process?

We need to do the closing entries to make them match and zero out the temporary accounts.

- Step 1: Close Revenue accounts.

- Step 2: Close Expense accounts.

- Step 3: Close Income Summary account.

- Step 4: Close Dividends (or withdrawals) account.

What are the 4 closing entries?

Recording closing entries: There are four closing entries; closing revenues to income summary, closing expenses to income summary, closing income summary to retained earnings, and close dividends to retained earnings.

What is included and excluded under the IFRS 16 definition of a lease?

The scope of IFRS 16 is broadly similar to IAS 17 in that it applies to contracts meeting the definition of a lease (see Section 3.), except for: (a) Leases to explore for or use minerals, oil, natural gas and similar non-regenerative resources; (b) Leases of biological assets within the scope of IAS 41 Agriculture …

Which item is not included in amount of the lease payment under IFRS 16?

A lessee may, but is not required to, apply IFRS 16 to leases of intangible assets other than licensing agreements for items such as motion picture films, video recordings, plays, manuscripts, patents and copyrights (which are excluded from the scope of IFRS 16).