Does the Fdcpa apply to original creditors

John Castro

Published Apr 07, 2026

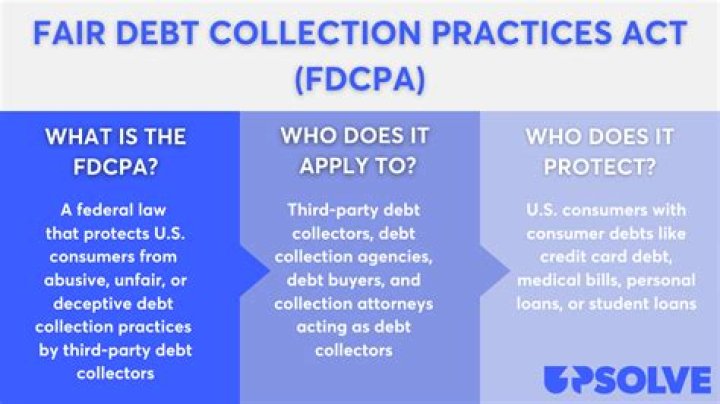

The FDCPA defines a “creditor” as the person or entity that extended you the credit in the first place (in other words, your original lender). Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn’t apply to your original creditor or its employees.

Does the FDCPA apply to first party collections?

By definition, creditors and first-party servicers are excluded from coverage because they are not “debt collectors” under the FDCPA. … These limits apply at the per-debt level, with the exception of student loans which may be aggregated by account number.

What debts does the FDCPA apply to?

The FDCPA applies only to the collection of debt incurred by a consumer primarily for personal, family, or household purposes. It does not apply to the collection of corporate debt or debt owed for business or agricultural purposes.

Does original creditor have to validate debt?

Collectors are required by Fair Debt Collection Practices Act to send you a written debt validation notice with information about the debt they’re trying to collect. … A statement that if you request information about the original creditor within 30 days, the collector must provide it.Who does the Fair Debt Collection Practices Act apply to?

The FDCPA only applies to third-party debt collectors, such as those who work for a debt collection agency. Credit card debt, medical bills, student loans, mortgages, and other kinds of household debt are covered by the law.

What laws are inplace to protect creditors?

In addition to the FDCPA, consumers in California are also protected by the California Fair Debt Collection Practices Act (CFDCPA). … There is additional legislation in California that also limits the potential actions of attorneys and law firm staff who attempt to collect debts for creditors.

Does FDCPA apply to banks?

v. Santander Consumer USA Inc., the United States Supreme Court held that the Fair Debt Collection Practices Act (“FDCPA”) does not apply to banks and other consumer finance firms that purchase and then collect on defaulted debt that they own.

Can a debt collector ask for more than the original debt?

Collection agency fees – what are legal? Debt collectors can charge you interest, up to the maximum amount outlined in the original contract. It’s generally listed as the “penalty rate” in credit card contracts and it can soar past 30 percent, depending on the creditor.Do collection agencies have to identify themselves?

Right to know the debt collector or debt collection agency Under the FDCPA, debt collectors are required to identify themselves when they attempt to collect a debt as well as note that any information you give them will be used in an attempt to collect the debt.

What happens if a collection agency refuses to validate debt?By law the collector has to notify you that you are entitled to ask for a validation of the debt within 5 days of contacting you about you owing money. … If they ignore you, you can sue them in small claims court for violations of the Fair Debt Collection Practices Act.

Article first time published onCan I pay the original creditor instead of the collection agency?

Even if a debt has passed into collections, you may still be able to pay your original creditor instead of the agency. … The creditor can reclaim the debt from the collector and you can work with them directly. However, there’s no law requiring the original creditor to accept your proposal.

Does FDCPA apply to judgments?

Some experts believe that unlawful detainer (eviction or landlord) judgments do not fall under FDCPA; the exception would be commercial tenancies. Unlawful detainers are summary proceedings where the only issue at hand is possession, and any judgment stemming from the underlying case is not consumer debt.

Does FDCPA apply to personal loans?

FAIR DEBT COLLECTION PRACTICES ACT. … Business debts are not included, but student loans, medical debt, credit card debt, and personal loans are all covered. The FDCPA applies to debt collectors, debt buyers, and law firms collecting upon a debt that did not originate with them.

What is the most common violation of the FDCPA?

- Continued attempts to collect debt not owed. …

- Illegal or unethical communication tactics. …

- Disclosure verification of debt. …

- Taking or threatening illegal action. …

- False statements or false representation. …

- Improper contact or sharing of info. …

- Excessive phone calls.

Are third-party debt collectors creditors?

Creditors are individuals or companies with whom you originally have the debt. … Only when you fall behind on payments owed and your debt goes into collections does it then get sold to debt collectors. At no time is a third-party debt collector classified as a creditor.

What does FDCPA mean?

Fair Debt Collection Practices Act.

Are debt collection agencies regulated?

All debt collection agencies are legally required to be regulated by the Financial Conduct Authority (FCA), which CPA are.

Can a bank be a debt collector?

The CFPB and the FTC Do. Share: Banks and other creditors, however, may still fall within the ambit of these July 28 Proposals because of the growing circuit split over whether a bank collecting on a debt acquired in default is a “debt collector” for purposes of the FDCPA. …

Is a collection agency a financial institution?

A collection agency is a business that is hired by a lender or other financial institution in order to collect debts from borrowers. … The collection agency will then do everything in their power to collect the full debt amount in order to make a profit.

What is the right of the creditor that is enforceable against a definite debtor?

Personal – jus ad rem, a right enforceable only against a definite person or group of persons.

What rights do creditors have?

Creditors’ Rights for Secured Claims Generally, secured creditors have rights based on a deed of trust, a mortgage, a security agreement on personal property like a car, or a judgment lien. Creditors with liens on property are entitled to receive value that is equal to the debt or the collateral—whichever is less.

What are the different rights which are available to the creditor?

- Unjust Enrichment (Quasi Contract) …

- Claim on Account. …

- NSF Checks. …

- Mechanic’s Liens. …

- Post-judgment Remedies. …

- Receivership. …

- Fair Debt Collection Practices Act. …

- Bankruptcy.

Do creditors have to tell you who they are?

A debt collector must tell you the name of the creditor, the amount owed, and that you can dispute the debt or seek verification of the debt. The CFPB’s Debt Collection Rule clarifying certain provisions of the Fair Debt Collection Practices Act (FDCPA) became effective on November 30, 2021.

Can you dispute a debt if it was sold to a collection agency?

When a debt has been purchased in full by a collection agency, the new account owner (the collector) will usually notify the debtor by phone or in writing. … That notice must include the amount of the debt, the original creditor to whom the debt is owed and a statement of your right to dispute the debt.

What is the statute of limitations on debt?

For example, in Ontario, British Columbia or Alberta, there is a two-year limitation period. This means that, while you still owe the money, creditors or debt collections cannot take you to court, they cannot seize your bank account, and they cannot take any other legal action against you.

Can I be chased for debt after 10 years?

In most cases, the statute of limitations for a debt will have passed after 10 years. This means a debt collector may still attempt to pursue it (and you technically do still owe it), but they can’t typically take legal action against you.

What should you not say to debt collectors?

- Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. …

- Never Admit That The Debt Is Yours. Even if the debt is yours, don’t admit that to the debt collector. …

- Never Provide Bank Account Information.

How many times can a debt be sold?

As of Late 2021, Federal Law Limits Debt Collector Calls The collector calls more than seven times within seven consecutive days. The collector calls within seven consecutive days of having had a telephone conversation about the debt.

How long does a creditor have to verify a debt?

Getting Verification of Debts The collecting creditor only has five days from first contact to provide a debt validation letter. According to the Consumer Financial Protection Bureau, entities attempting to collect a debt must provide you with certain information.

What is a 609 letter?

A 609 Dispute Letter is often billed as a credit repair secret or legal loophole that forces the credit reporting agencies to remove certain negative information from your credit reports. And if you’re willing, you can spend big bucks on templates for these magical dispute letters.

How can I get out of debt collectors without paying?

There are 3 ways to remove collections without paying: 1) Write and mail a Goodwill letter asking for forgiveness, 2) study the FCRA and FDCPA and craft dispute letters to challenge the collection, and 3) Have a collections removal expert delete it for you.