Can a 457 plan be Roth?

Christopher Anderson

Published Feb 19, 2026

Can a 457 plan be Roth?

In addition to potentially tax-free distributions in retirement, the ability to make Roth contributions to your 457 plan has the following benefits: Eligibility at all income levels – Unlike Roth IRAs, everyone with earned income is eligible to make Roth contributions to their employer’s 457 plan.

What is the difference between a Roth IRA and a Roth 457?

How does the Roth 457 differ from a Roth IRA? Roth IRA contributions are limited to $6,000 in 2020 (or $7,000 if you are age 50 or over) compared with $19,500 for the Roth 457 (or $26,000 if you are age 50 or over). You can contribute more on an after-tax basis to your Roth 457 than to a Roth IRA.

What happens to my 457 B when I retire?

Once you retire or if you leave your job before retirement, you can withdraw part or all of the funds in your 457(b) plan. All money you take out of the account is taxable as ordinary income in the year it is removed. This increase in taxable income may result in some of your Social Security taxes becoming taxable.

What is a 457 B Roth plan?

A 457(b) plan is an employer-sponsored, tax-favored retirement savings account. With 457(b) plans, you contribute pre-tax dollars, which won’t be taxed until you withdraw the money. A 457(b) retirement plan is much like a 401(k) or 403(b) plan.

How does a 457 Roth work?

A 457 plan contribution can be an effective retirement tool. The Roth 457 plan allows you to contribute to your 457 account on an after-tax basis – and pay no taxes on qualifying distributions when the money is withdrawn. Use this calculator to help determine the best option for your retirement.

Can you contribute to a 457 after retirement?

There are two types of catch-up contributions: If you are within three years of retirement, the 457 plan gives you the opportunity to make up for years in which you did not make the maximum contribution. Individuals age 50 or older may contribute additional amounts above the “applicable deferral limit” for the year.

Is a Roth 457 a good idea?

A 457 plan contribution can be an effective retirement tool. The Roth 457 plan allows you to contribute to your 457 account on an after-tax basis – and pay no taxes on qualifying distributions when the money is withdrawn.

Can you use 457 to buy a house?

It is true that borrowing from a 457(b) plan may be used for first-time home buying. However, it must be a loan from the plan, not a withdrawal. Even then, there are certain restrictions that apply, which may cause some or all of the loan to be treated as a distribution subject to the 10 percent penalty.

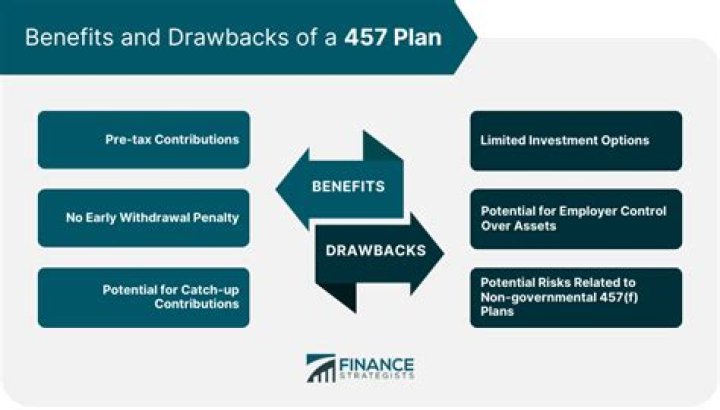

What are the benefits of a 457 plan?

Contributions to a 457 are taken from your gross income, reducing your taxable wages. Your money then grows tax-deferred until you withdraw it, at which point it will be taxed as income. And because, like a 401(k), the deductions are automatic, a 457 offers one of the more painless ways to save for retirement.

How do I make Roth contributions to my 457 retirement plan?

You should contact your employer or MissionSquare Retirement to confirm that your plan permits Roth deferrals. Provided that you have already enrolled in the plan, you can use the 457 Deferred Compensation Plan Amount of Deferral Change Form to start making Roth contributions.

What are the tax benefits of a 457(b) retirement plan?

There are significant tax advantages for participants in a 457 (b) plan: Contributions to a 457 (b) plan are tax-deferred. Earnings on the retirement money are tax-deferred. Can a 457 (b) plan include designated Roth accounts?

Is there a penalty for early withdrawal from Roth 457 plan?

Early withdrawals from a Roth 457 plan are also not subject to a ten percent penalty. However, early withdrawals ARE subject to ordinary income taxes. Withdrawals from a Roth 457 plan after age 59 1/2 are both tax-free and penalty free.

Do 457S and Roth IRAs have required minimum distributions?

Do 457s and Roth IRAs Have Required Minimum Distributions? Required minimum distributions (RMDs) apply to all employer-sponsored retirement plans, including 457s. Once you hit age 72, you have to start taking withdrawals or you risk having to pay a steep 50% tax penalty. 2 (The SECURE Act of 2019 increased the age to 72.